Expenses are inevitable, and so are emergencies. But, unfortunately, there are millions of individuals for whom the costs and unexpected events nail them to the wall. And they end up depending on either payday loans or installment loans to survive.

In addition, the most significant percentage of workers depends on paycheck to paycheck, which makes them unable to save a penny. Here are some dangers of relying on paycheck alone.

Maybe you have been wondering what kind of loan you should apply for to sort out your emergencies. You could be contemplating between a payday loan and an installment loan. But first, I would like you to know the difference between both of them.

The differences between payday loans and installment loans

I’m going to analyze for you the different ways in which payday loans and installment loans differ.

Definition

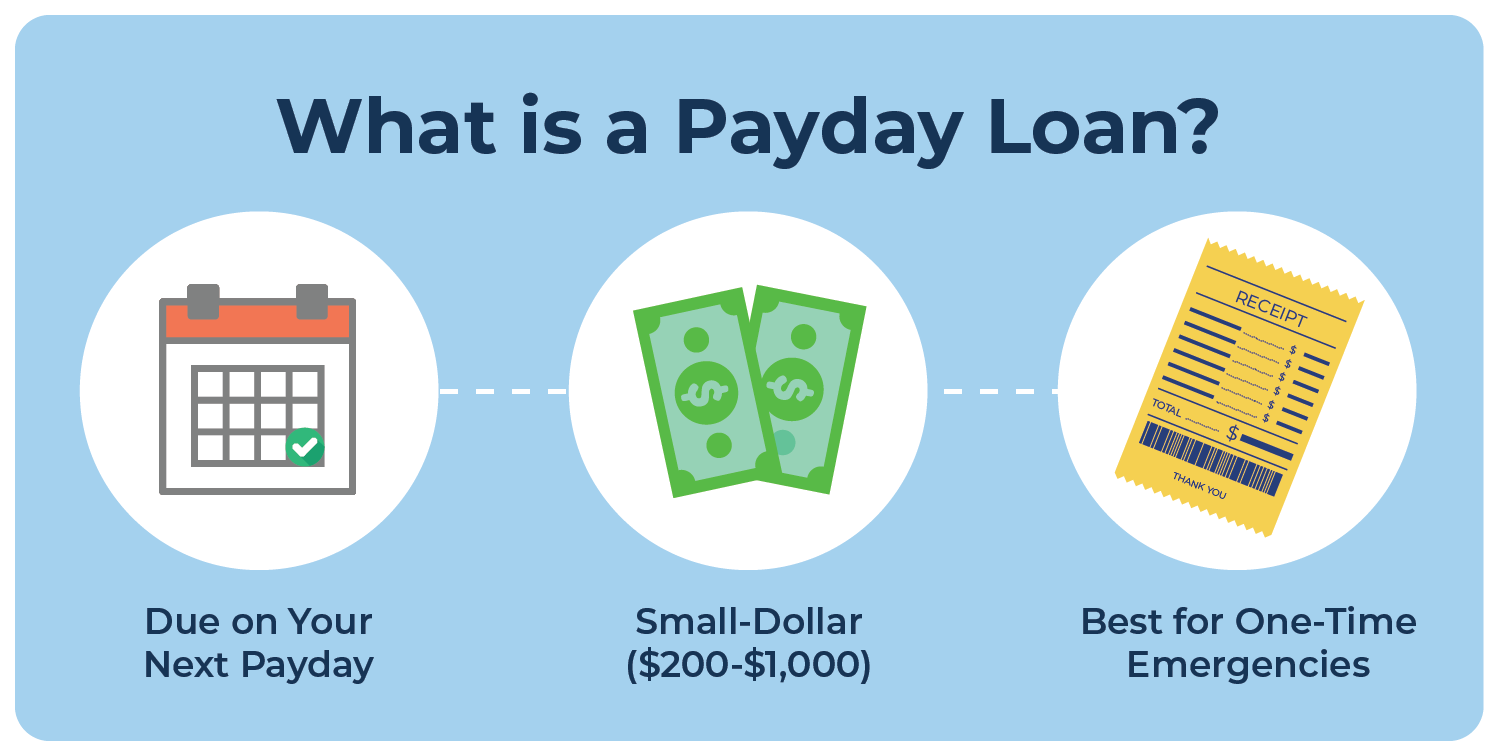

Payday loans are loans characterized by a small amount of money that a borrower gets from a payday lender and payback in the next paycheck.

Installment loans are loans ranging from mortgages, car loans, business loans, and also personal loans. The borrower does not repay the whole amount at once but in smaller segments and longer.

Maximum loan amount

Payday loans have smaller limits of the loan amount, usually going up to $1,000. On the other hand, installment loans can go up to hundreds of thousands of dollars. This aspect makes installment loans more suitable for doing long-term projects that require vast amounts of cash.

Repayment period

The repayment of payday loans can only be for two weeks, usually paid during the next paycheck. This criterion means that only employed individuals can access payday loans.

On the other hand, lenders divide installment loans into small installment segments and spread them over longer.

For instance, if you borrow a $100,000 loan with an interest rate of 15% p.a, and repay in two years (24 months). The interest will be 15/100*100,000= 15,000. The total amount will be 100,000+15,000=115,000. So, take 115,000/24months=4791.67. You will be paying $ 4791.67 per month for 24 months.

The borrower will pay the loan either monthly, bi-monthly, or even semi-monthly for the agreed time.

The APR

The APR for payday and installment loans is quite significantly different. However, payday loans have very high interest rates since they are short-term loans with no security. The APR for payday loans is 391% or even higher, which makes them very expensive.

On the other hand, installment loans have lower interest rates ranging from 10% to 15%.

Credit checks

For payday loans, there are no credit checks for you to qualify for a loan. Instead, the payday lenders depend on that you are employed, and you can repay the loan. They also rely much on the huge interest rates to cover any possible case.

For you to qualify for an installment loan, the lenders conduct a credit check to know your creditworthiness and determine what to give you. Since the loan amount is high and the repayment period is also high, lenders must conduct credit checks.

Approval time

Payday loans are approved faster within 24 hours. So if you need little cash for an emergency, then you may consider getting a payday loan. Some other online lenders like Vivapayday loans can even approve your loan within 2 minutes.

Installment loans can take a while before the lender approves due to the lengthy procedures involved. But they are suitable for flexible payment plans. So if you don’t want more pressure when repaying a loan, you better go for the installment loans.

The terms

In payday loans, you will have to access the lender to deduct all the repayment after the next paycheck. Instead, you can give them a post-dated check.

As for the installment loans, you pay the agreed amount of installment at the arranged time.

Eligibility criteria

To qualify for payday loans, you will have to be:

- Be at least 18 years

- Have an active checking account

- Provide proof of steady income

- Provide actual address and identification documents

On the other hand, installment loans consider your identity, your credit score, and the lenders may also ask you to provide collateral to qualify for a loan.

ALSO CHECK: Top 5 Apps That Save Money Fast

The bottom line

Now you know the difference between a payday loan and an installment loan. First, always consider the reasons you need a loan. From there, you will see whether you need a payday loan or an installment loan. Just a reminder, always take a loan that you need, do not take loans that you will have trouble paying.